Tesla’s in-house insurance program has quietly evolved into something more strategic than a standard coverage offering. By tying FSD engagement directly to premium calculations, the company is building a financial structure where automation pays—literally. For Model S/X, and Cybertruck owners, the resulting savings can offset the FSD subscription cost entirely.

Underlying logic isn’t complicated. Tesla Insurance prices risk based on real-time behavioral data, and FSD-assisted driving consistently scores better than human operation. Starting with FSD v13, that preference became explicit: the more miles logged under FSD, the more favorable the premium calculation.

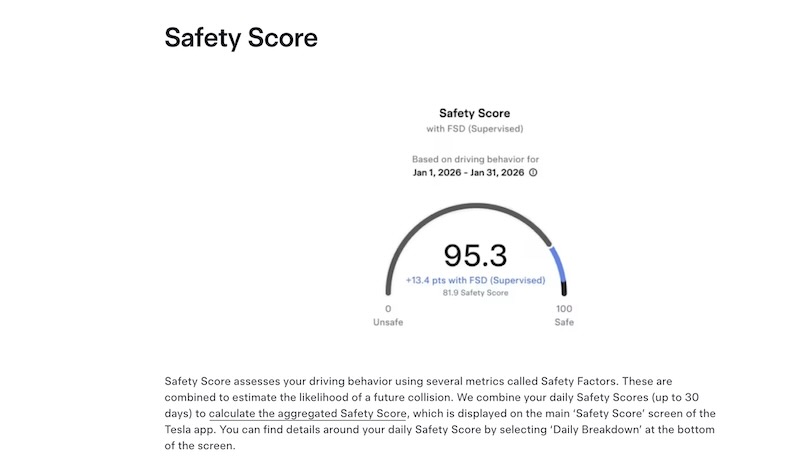

FSD v14 formalizes this further. Safety Score v3.0 now assigns a perfect 100 to every mile driven under “FSD Supervised” mode. That ceiling score feeds directly into the lowest available premium tier. Owners reporting early results are citing cuts of up to 30%, a significant shift from a single software update.

Timing matters here. Existing policyholders receive Safety Score v3.0 at their next renewal cycle, with advance notice arriving roughly two months prior. New policies in Arizona, Illinois, Indiana, Tennessee, Texas, and Virginia activate the scoring system immediately.

California isn’t on that list, and the exclusion is regulatory rather than logistical. Proposition 103 restricts auto insurance pricing to three primary factors: driving record, annual mileage, and years of experience. Real-time telemetry data, hard braking events, nighttime driving patterns, FSD engagement status, requires separate regulatory approval to influence rates. Privacy considerations compound that barrier, leaving Tesla’s most populous U.S. market outside the program for now.

Tension this creates isn’t new. Usage-based insurance models have always bumped against privacy frameworks, and California’s oversight structure is among the strictest in the country. Regulators prioritize transparency, Tesla prioritizes behavioral data. Those two positions don’t currently align.

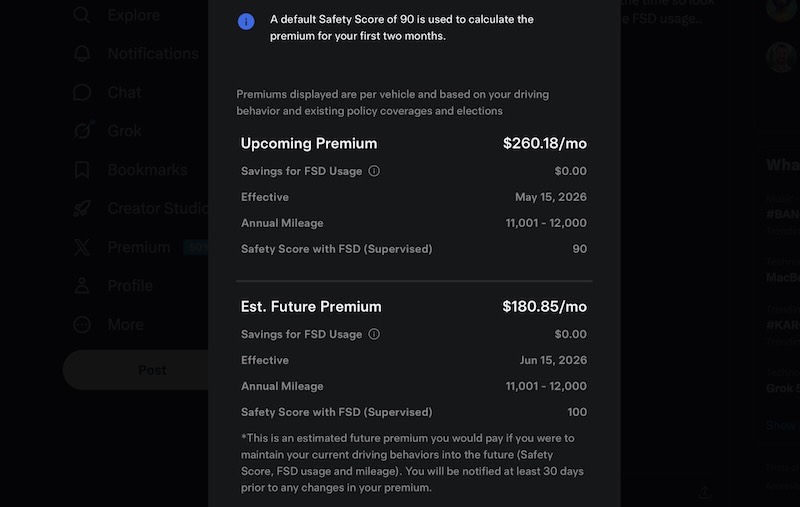

One Model Y Performance owner in Arizona shared updated projections after gaining Safety Score v3.0 access, noting immediate downward movement in premium estimates tied directly to consistent FSD usage. The practical outcome: annual insurance costs for a Model Y Performance dropping to approximately $2,170, a competitive figure for a high-performance EV by any standard.

That number matters beyond the individual policy. It signals that Tesla FSD insurance savings aren’t marginal adjustments, they represent a structural repricing of risk for drivers who commit to the system.

Tesla isn’t running an insurance experiment in isolation. Program functions as a feedback loop: better FSD performance lowers risk scores, lower risk scores reduce premiums, and reduced premiums incentivize higher FSD adoption. Each variable reinforces the others.

As the autonomy stack matures, that loop tightens. What started as a pricing model is gradually becoming a data-driven redefinition of how automotive risk gets measured, who benefits when the algorithm takes the wheel. With Tesla FSD insurance savings, real question isn’t whether the math works. It’s whether drivers are ready to let their car write their premium.

Related Post

Tesla Insurance Launches in Florida with Safety Score-Based Pricing

Tesla Insurance Launches in Minnesota – Now Available in 12 States

Tesla FSD V14.3 Released: Faster Reactions, Smarter Vision and Major RL Upgrades